Owning a home is a milestone that anyone will be proud of. For some, it’s a sign of financial independence. For others, it’s a status symbol.

Despite the financial challenges due to the pandemic in the past few years, more Filipinos sought opportunities to own a house last year, which resulted in the Pag-IBIG Fund releasing a record-high ₱57.07 billion worth of home loans in the first half of 2023. [1]

With low interest rates and longer repayment terms, the Pag-IBIG Housing Loan is one of the more affordable and flexible home financing schemes in the Philippines. If you’re planning to apply for this home loan, we’ve come up with a simple primer that covers the program’s basics. We also have Pag-IBIG housing loan tips to increase your chances of getting approved.

Launched in 1978, the Home Development Mutual Fund, or the Pag-IBIG Fund, is a government-owned agency that manages the national savings program and offers affordable house financing to its members. With a repayment term of up to 30 years, this works as a more flexible alternative to bank and in-house home financing schemes.

You can borrow up to ₱6 million for any of the following purposes:

_1200x350.png?width=367&height=107&name=UNOBank_Loan_-_Home_Improvement_(Apr_2024)_1200x350.png)

Need extra funds for your home improvement? You don't have to delay it if you're short on cash. Simply get a cash loan from UNO Digital Bank via Moneymax. Enjoy a fast application and approval process, plus instant loan disbursement!

Whether it's a simple appliance upgrade or a home remodeling project, UNOBank got you covered with its loan amount ranging from ₱10,000 up to ₱500,000. Apply for an #UNOnow Loan today!

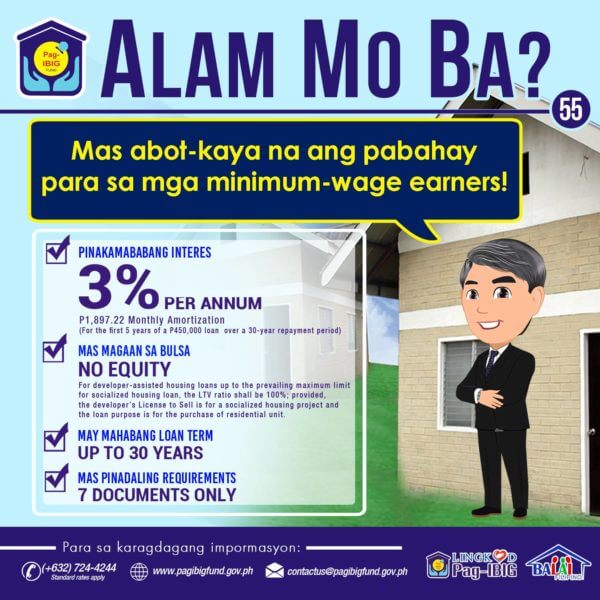

It’s important to note that Pag-IBIG has a separate housing loan program for minimum-wage and low-income earners, aptly called the Pag-IBIG Affordable Housing Loan Program.

Under this program, members who earn up to ₱15,000 a month within the National Capital Region (NCR) or ₱12,000 outside the NCR can apply for a housing loan. Pag-IBIG offers a subsidized interest rate for home loans up to ₱580,000 in socialized subdivision projects and special low rates for loans up to ₱750,000 in socialized condominium projects. [2]

The Pag-IBIG Housing Loan interest rates are some of the lowest on the market today. Your rate will depend on your preferred repricing period.

Here are Pag-IBIG’s interest rates as of July 2023: [3]

| Repricing Period | Interest Rate |

| 1-year fixing | 5.75% |

| 3-year fixing | 6.25% |

| 5-year fixing | 6.5% |

| 10-year fixing | 7.125% |

| 15-year fixing | 7.75% |

| 20-year fixing | 8.50% |

| 25-year fixing | 9.125% |

| 30-year fixing | 9.75% |

What is a repricing period, you ask? The repricing period refers to the period where the indicated interest rate takes effect. After the said period, your interest rate will change. It will either go up or down, depending on the economy at the time of the repricing.

Say you go for a loan with a repricing period of three years. Looking at the table above, this means that you will pay a Pag-IBIG Housing Loan interest rate of 6.25% for three years. After three years, Pag-IBIG will conduct an evaluation and change the interest rate depending on the prevailing market conditions.

On the other hand, the Pag-IBIG Affordable Housing Loan entitles qualified members to special subsidized interest rates. Borrowers can enjoy an interest rate of 3% for the first five years of the loan term and a 6.5% interest rate during the first 10 years of the loan.

You can pay for your loan for up to 30 years. However, the payment period should not exceed the difference between the age of 70 and your current age.

The Pag-IBIG housing loan application process isn’t easy, though—and neither is getting approved. It will take time, energy, and even money to comply with all the eligibility and documentary requirements.

Here’s everything you need to know:

You are eligible for a Pag-IBIG Housing Loan if you satisfy the following:

Here are the Pag-IBIG Housing Loan requirements for 2024:

For the complete list of requirements per loan purpose, visit the Pag-IBIG website. [4]

How to apply for a Pag-IBIG Housing Loan? Follow these six steps:

%201200x350%20CTA-1.png?width=376&height=110&name=UB%20PL%20Generic%20Ad%20(Sep%202023)%201200x350%20CTA-1.png)

.png?width=300&height=200&name=Pics%20for%20blog%20-%20600x400%20(38).png)

According to Pag-IBIG Citizens Charter 2023, [5] the Pag-IBIG Housing Loan approval time is around 20 working days.

After you submit your complete documents, the Pag-IBIG Housing Loan takes around 17 processing days.

Wondering how many days it takes for the Pag-IBIG Housing Loan release? If they approve your housing loan, they will release the proceeds three days after you submit the required post-approval documents.

Here's how to increase your chances of getting approved for a Pag-IBIG housing loan.

Any missed payment can ruin your chance of getting approved for a new loan. Pag-IBIG declines housing loan applications from borrowers with unpaid multi-purpose loans or foreclosed/canceled housing loan accounts with the agency. Check your existing Pag-IBIG loan accounts, if any, and pay off any outstanding loans before you apply for a new housing loan with Pag-IBIG.

Thinking of quitting your job? Job hopping will hurt your chances of getting approved—more so if you switch to a lower-paying job or a career with irregular income.

Pag-IBIG will check your employment history to assess if you’re financially stable enough to handle all your monthly mortgages. Your employment tenure proves your income stability.

Ideally, you should have a steady income source for at least two years. You’re better off sticking with your current job if you plan to apply for a loan with Pag-IBIG soon.

Think of the credit score as a representation of your trustworthiness and responsibility when handling loans and other financial obligations. Any delinquency in your credit card and loan payments is a red flag to lenders. If you have a bad track record of repayments, you’re less likely to get approved

Review your credit report at least a year before applying for a housing loan with the Pag-IBIG Fund. This will give you enough time to correct any errors and improve your credit score. You can access your credit report through the Credit Information Corporation [6] or one of its accredited credit bureaus.

Qualified Pag-IBIG members can borrow up to ₱6 million for financing a home, but that doesn’t mean you should go for the maximum amount. After all, the agency will still evaluate if you’re actually qualified. The same level of verification and evaluation will also apply even if you’re borrowing money worth less than ₱6 million.

Consider your financial situation and capacity. Can you pay the principal and interest with your monthly income?

Pag-IBIG has a housing loan affordability calculator [7] that quickly computes how much you can borrow and pay in monthly amortization. The calculation is based on your income, your chosen loan term and fixed pricing period, and the estimated value of the property you want to buy. It's also useful if you want to know the required gross monthly income for the amount you want to borrow.

Making a huge down payment proves your financial stability. It’s also a win for you since you’ll be borrowing a lower amount from the Pag-IBIG Fund, which in turn may mean lower monthly amortizations.

Ideally, pay at least 20% of the property’s value. If you can pay more, better.

If you’re determined to raise a higher down payment and willing to delay your purchase, consider creating another stream of income, such as side gigs or a small business. If you have a windfall, such as an unexpected inheritance, commission, or bonus, use it to fund your down payment.

Your Certificate of Employment and Compensation (CEC) can make or break your housing loan application. This income document, which shows your gross monthly income and other monetary benefits, proves your capacity to repay your loan.

Your CEC must contain accurate and updated information. For instance, if you recently got a raise, it should indicate your latest monthly salary. If you’re receiving de minimis benefits or non-taxable allowances, request your HR manager to include such details as well.

If your income is low, it’s hard to qualify for most home loans in the Philippines. But fortunately, you may qualify for Pag-IBIG’s Affordable Housing Loan Program.

As mentioned earlier, this program offers subsidized interest rates and special low rates. If your application is approved, your monthly payments might be more manageable.

To keep track of which documents you’ve already secured and those you still need to work on, create a checklist of all housing loan requirements and their corresponding status on a spreadsheet.

Double-check the accuracy of the information in your documents to avoid delays. Also, compile your documents in one folder or envelope to ensure everything’s in place when you submit the housing loan requirements to Pag-IBIG.

Borrowers who want to purchase properties under negotiated sale [8] are required to make a bid by submitting an Offer to Purchase in a sealed envelope. The borrower with the highest bid gets the chance to purchase the property. Pag-IBIG provides a list of homes under this category with a specified bidding period.

Making a bid can be very exciting, but this should be done with much thought. Visit the showcased property first—most of the houses under negotiated sale are fully constructed but either abandoned or in need of renovation.

Here are a few things to remember before making the offer:

Homes under negotiated sale can also be purchased with a discount depending on your chosen mode of payment which you’ll also indicate when bidding.

It can be stressful, not to mention painful, but that doesn’t mean your dream of owning a home is entirely shattered.

Here’s another set of Pag-IBIG housing loan tips for dealing with a denied application.

Pag-IBIG allows you to apply with a family member or two for a single home loan. Relatives up to the second degree are accepted, so you can apply with your spouse, parent, sibling, in-law, or cousin. Since their income will be added to yours, the application has a better chance of getting approved.

However, be careful when asking someone to co-sign a loan with you. Not everyone in the family will agree to be responsible for any unpaid debts you make.

Choose a co-borrower with whom you’ll share the new home and who’s genuinely willing to help you out. Also, get one who can fulfill all the co-borrower requirements.

While scouting for a new home, you might stumble upon your dream house. But can you actually pay the monthly amortization without any struggle?

If you want your application to be approved, buy a home you can afford. Even if you purchase property that doesn’t fit your idea of a dream home, you’ll sleep better at night knowing that you have a roof over your head and can afford to pay your monthly amortizations.

Keep exploring, and you’ll find thriving locations and communities with cheaper properties. If you’re not in a rush to move into a new home, consider buying a pre-selling property.

While the housing loan from Pag-IBIG is the top-of-mind choice of Filipino homebuyers, there are other ways to finance your dream home.

Bank financing is another viable way to borrow money for a home purchase. Home loans from banks offer competitive rates (around 5% to 6%). But like the Pag-IBIG Fund, banks have strict requirements and credit evaluations for borrowers.

Consider in-house financing as well. Instead of going through a third-party lender, a homebuyer directly deals with the seller or property developer to avail of a home loan.

The requirements are minimal, and the process is simple and straightforward. However, in-house financing has higher interest rates and shorter payment terms than other housing loan providers.

The Pag-IBIG Housing Loan tips above will help you increase the odds of your application’s success. But if you have other questions, you may find the answers here.

Pag-IBIG sees to it that your monthly repayment will not exceed 35% of your monthly income. If your monthly installment for the housing loan is ₱7,000, then your salary should be higher than ₱20,000.

Find out how much you can afford for the monthly amortizations. This way, your budget will not be significantly affected.

Try looking for other sources of income. Pag-IBIG considers other types of income sources, including freelance gigs. Just submit proof of regular remittances from your freelance employers for the last 12 months.

Submit these documents if you don't have a Certificate of Employment, or if you have a low income:

Does Pag-IBIG check credit scores? Pag-IBIG’s Housing Loan credit investigation aims to see if borrowers have loan delinquencies. Outstanding debts from banks or other lenders will not affect your loan application, as long as all your total loan repayments can still be covered by your regular income and you’ve paid your dues on time.

Pag-IBIG allows a lump sum payment of contributions and savings. So if you have enough cash on hand, then you can make a one-time payment to comply with this requirement.

You can repay your Pag-IBIG Housing Loan via the following methods:

Pag-IBIG has a list of accredited collection partners where you can settle your payments:

Owning a real estate property seems like an elusive dream, but you have the Pag-IBIG Fund to back you up financially. The application process can be complicated and demanding, but remember the benefits: a lower interest rate and a convenient payment term.

If you want to fast-track your application process and get approved, keep the above-mentioned Pag-IBIG housing loan tips in mind. Get in touch with Pag-IBIG personnel for other details, such as additional documentary requirements.

If you get rejected, don’t lose hope. There are other home financing options in the Philippines, such as housing loans from banks, that you can avail of at competitive rates:

Provider Loan AmountMonthly Add-on Rate

Minimum Annual Income

Approval Time

UnionBank Personal Loan![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

Sources:

Venus has almost 20 years of combined experience in content marketing, SEO, corporate communications, and public relations. Most of her career was spent creating informative articles on personal finance and digital marketing. She also invests in stocks, mutual funds, VUL, and Pag-IBIG MP2. Venus graduated cum laude with a Journalism degree from the University of the Philippines Diliman. A hardcore Hallyu Tita, she loves bingeing Korean shows on Netflix while bonding with her cats. Follow Venus on LinkedIn.